back

The impact of your credit score on securing an owner occupied commercial real estate loan

01-2023

When deciding whether you qualify for an owner-occupied commercial real estate loan, your credit score is a key factor. While a low credit score can make it challenging to get financing, a good credit score can open up a world of opportunities. We’ll look at how your credit score affects getting approved for an owner-occupied commercial real estate loan in this blog post, as well as what you can do to increase your chances.

Let’s define what an owner-occupied commercial real estate loan means first. This kind of loan is intended for people or companies who want to buy or refinance a piece of real estate that will serve as their main place of business. This can apply to warehouses, retail stores, office buildings, and other kinds of commercial real estate.

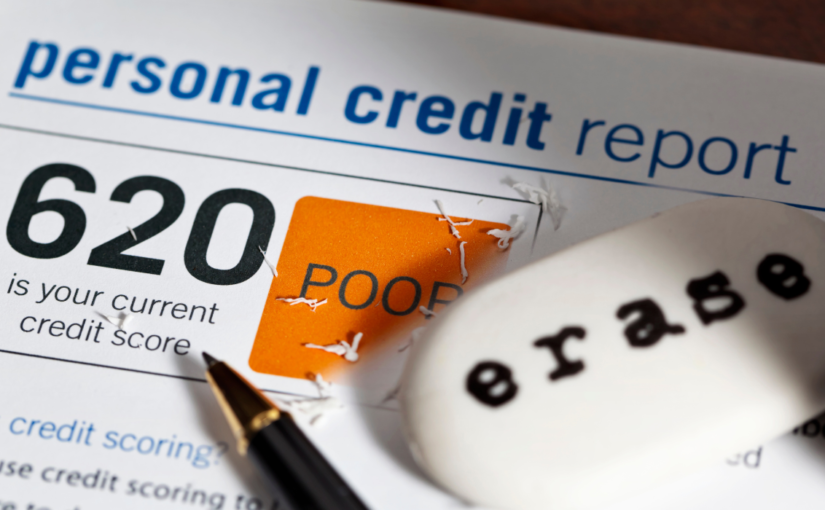

Your credit score is one of the most crucial factors that lenders will take into account when deciding whether to grant you an owner-occupied commercial real estate loan. Based on data from your credit report, a credit score is a numerical representation of your creditworthiness. Your chances of getting a loan approved and the terms you’ll be given increase with your credit score.

In the United States, Experian, Equifax, and TransUnion are the three main credit reporting companies. They are in charge of gathering and disclosing credit data from a variety of sources, including banks, credit card companies, and other financial institutions. Your credit history, including how much you owe and how well you’ve paid your bills in the past, is among the details in your credit report.

The data in your credit report is used to determine your credit score. The FICO score, which ranges from 300 to 850, is the most frequently used credit score. In general, a score of 720 or higher is regarded as excellent, while one of 650 or lower is regarded as subpar.

A credit report from one of the three major credit reporting agencies will typically be requested by the lender when you apply for an owner-occupied commercial real estate loan. They’ll assess your creditworthiness and decide whether to approve your loan application using the information you provide.

You’ll be given better terms and have a higher chance of loan approval if you have a high credit score. You might, for instance, be eligible for a lower interest rate, which would mean lower monthly payments. However, if your credit score is low, you might be turned down for a loan or given less advantageous terms.

Therefore, if your credit score is low, how can you increase your chances of being approved for an owner-occupied commercial real estate loan? Here are some pointers to raise your credit score:

- Punctually pay your bills. It’s crucial to make sure that you pay all of your bills on time because missed payments can significantly harm your credit score.

- Keep the balances on your credit cards low. Keep your credit card balances as low as possible because carrying a high balance can also harm your credit score.

- Challenge any mistakes found on your credit report. Your credit report may occasionally contain errors that have a negative effect on your credit score. You can dispute any errors you find on your credit report with the credit reporting agency and ask that they be fixed.

- Don’t apply for credit too frequently. A hard inquiry is made on your credit report each time you apply for credit, which can harm your score.

- Look for a co-signer. If you can’t get a loan approved on your own, a co-signer with good credit might be able to help you out.

You can raise your credit score and raise your chances of being granted a loan for owner-occupied commercial real estate by implementing the advice in this article. It’s important to keep in mind that raising your credit score takes time, so you should start working on it well in advance of your intended loan application date.

The property itself is a crucial factor that lenders take into account when assessing your loan application. The property’s condition and value as an investment will be scrutinized by the lender. Additionally, they’ll want to know that the property will bring in enough money to pay the loan. In order to determine whether you can afford the loan payments and any necessary property repairs, lenders will also look at your financial statements, including your income statement, balance sheet, and cash flow statement.

In conclusion, your ability to obtain a loan for owner-occupied commercial real estate is significantly influenced by your credit score. While a low credit score can make it challenging to get financing, a good credit score can open up a world of opportunities. You can increase your chances of being granted an owner-occupied commercial real estate loan by working to raise your credit score and making sure the property is a wise investment.

F2H Capital Group is a debt advisory firm specializing in negotiating the best terms for your commercial real estate projects. The company offers a range of financial products and services, including fixed loans, bridge loans, and construction loans across all asset types. Please contact us for any of your financing needs.